2 – Visa and MasterCard have completely permeated the Canadian Payment System

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

Since Visa and MasterCard largely increased credit card transaction fees in 2008, retailers across the board have been urging Ottawa to limit these abusive costs by imposing a regulatory rate cap, as in Europe.

However, 10 years later, Ottawa still rejects this solution, preferring cosmetic reductions through voluntary agreements. Why?

In a series of articles entitled “The Secret Memos of Bill Morneau”, DepQuébec tries to understand the Federal government point of view on this issue after having obtained for the first time highly secret and sensitive ministerial memos through the access to information Act.

Today, for the series second part, we look at the growing share of credit card transactions within the Canadian payment system.

In the cosy Parliament room, a relaxed and smiling Bill Morneau enjoys small talk with a handful of retailer association representatives, putting them at ease.

Then, after a while, they all start laying down their case, one by one, switching from French to English and vice versa, each trying to illustrate the misery, injustice and immorality of credit cards fees.

Hoping to capture the Minister’s imagination, one of them comes up with a shocking image.

“Mr. Morneau, as a businessperson yourself, you can certainly understand the frustration and anger of a convenience store owner selling gas, working seven days a week from 7 am to 11 pm and earning only 3 cents per liter of gas, no matter at what price it is sold. Should the price goes up to $1.50 a liter, a customer paying with a VISA privilege card at 2% means that his 3 cents gross profits completely vanish into nothingness, sucked in by the vacuum of interchange fees so that he ends up with nothing!”

Nothing like zero, zilch or total emptiness.

Welcome to the “assessment of the fees charged by credit card networks and review of the fee reductions’ effects” as the government puts it, an informal round of consultation launched by Finance Canada in September 2016.

According to one of Bill Morneau’s secret memos dated June 20, 2017, the purpose of this assessment which ended that same month was to “determine whether there is an appropriate balance between the costs and benefits of credit card transactions for merchants and consumers and to review the effects of the volontary fee reductions”.

Focused, Mr. Morneau listens to the arguments, frowns and sympathizes. The hard labour of retailers is indeed siphoned off by credit card transaction fees that don’t make sense to them, providing nothing tangible in return. In addition, they are powerless to negotiate them, having no leverage to oppose large banks and credit card companies nor any alternative.

However, the minister’s deputy, sitting on his right, remains silent. His perspective is different.

If, on the one hand, there is indeed the reality of retailers, on the other hand, there is the reality of consumers whose expenses are the country’s main economic driver, supporting businesses and employment from coast to coast.

Never without my card

Although heavily redacted, Bill Morneau’s secret memos are revealing by what they contain and omit. And fortunately, the substantive background information presented in these documents generally get through the censors scissors.

By indicating which data is key to the government, they are revealing what it considers essential.

And what do we see? An analysis of the 5 to 6 billion extorted from retailers each year? Not at all.

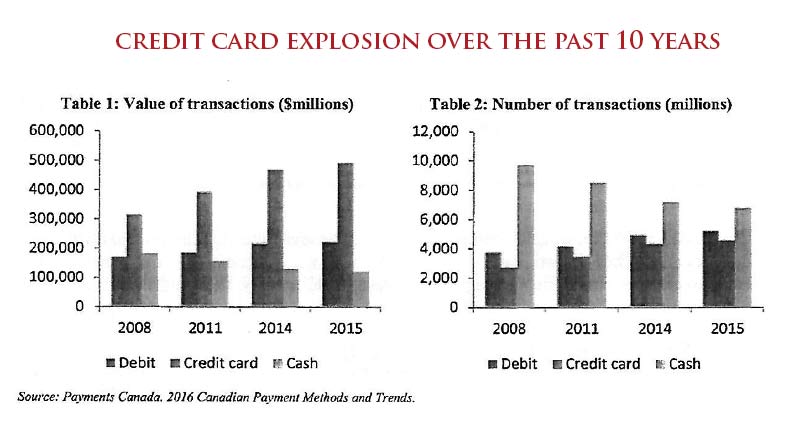

Rather, a dramatic portrait of the exponential growth that credit card payments have been enjoying in Canada for the past 10 years.

Let’s put it simply: according to the secret memos, Canadians can’t live without their credit card … they have become completely addicted to them!

For a few billion less

We know from the outset that capping credit card fees would save retailers 5 or 6 billions in costs (and consumers as well via an overall price reduction).

But the question the government seems obsessed with is what would be the impact on the overall consumer spending once the rewards are mostly gone.

Indeed, since VISA and MasterCard opened the tap of rewards in 2008 and started offering all sorts of new points, privileges and so forth, consumers have eagerly adopted them and always been hungry for more and more.

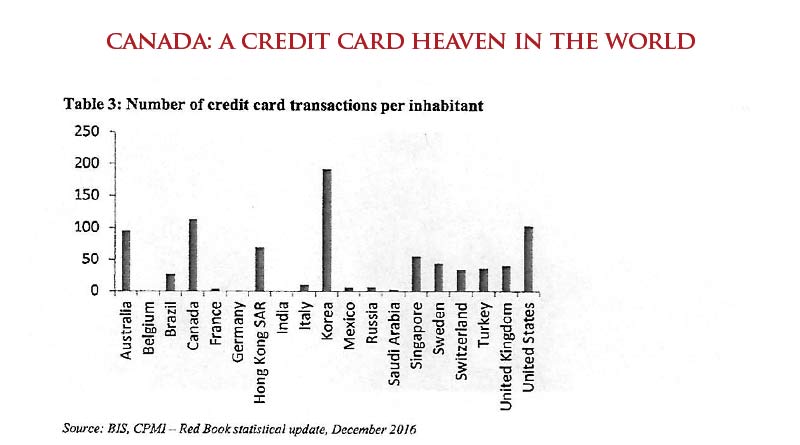

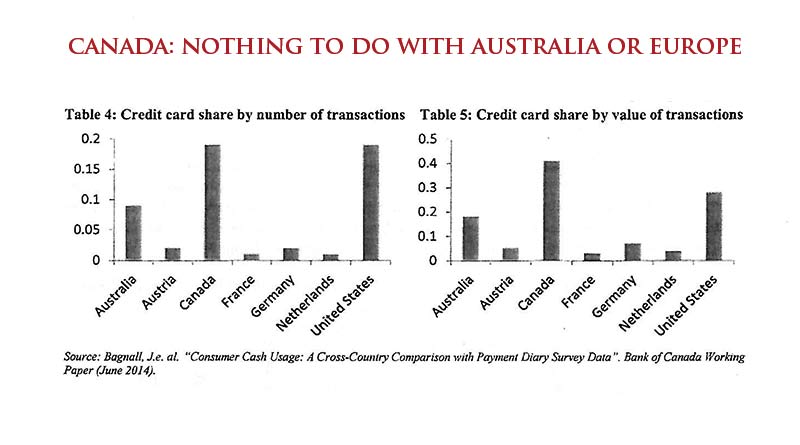

Retailers like to remind the government that Europe and Australia have legislated to cap credit card fees. What they do not know, however, is that Canada is far more infatuated with card payments than anywhere else in the world except for South Korea, a country where interchange fees are non-existent.

The love of Canadians for their credit card is, in fact, almost unique in the world. The country far exceeds the United States in terms of the average value per transaction, a quite revealing clue of their strong attachment.

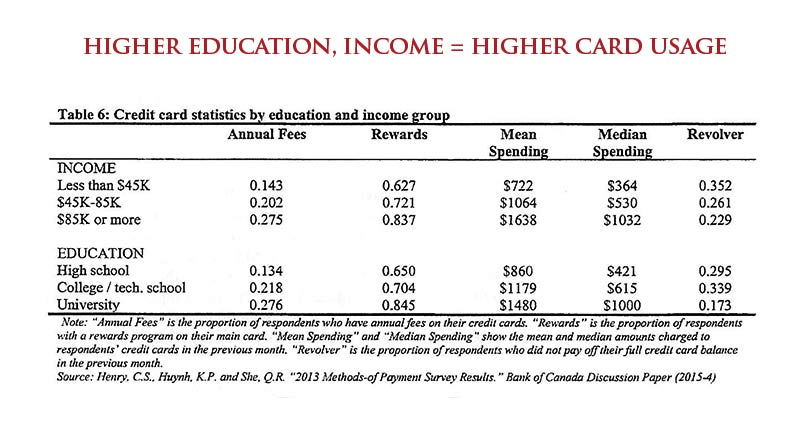

Yes, but still remains the risk that credit cards pose in encouraging consumers to spend beyond their means! Well, not really it seems. The data shown in the secret memos reveal a strong positive correlation between education, income and card usage. And most pay their balance in full at the end of the month!

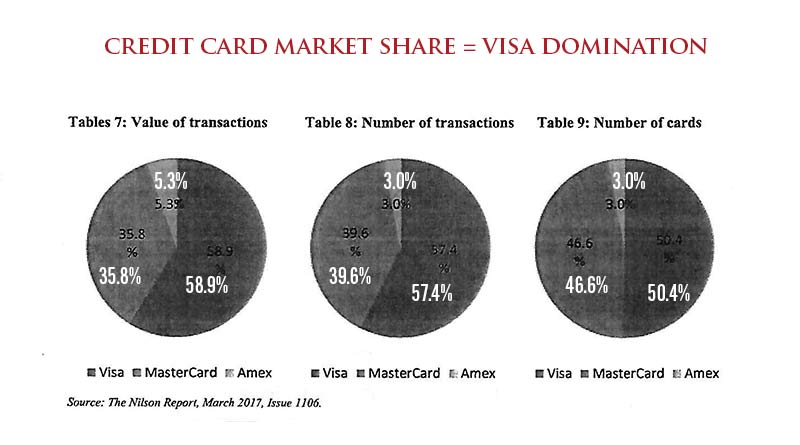

As for the existence of a duopoly, that is a fact. Visa and MasterCard share almost the entire market and surprisingly, MasterCard has almost as many cards in circulation as VISA.

A feared popularity

The credit card companies’ objective to become an integral part of our economy and payment system seems to have been largely achieved.

In 2008, their decision to multiply privilege cards had the effect of dumping billions in interchange fees on retailers. On the other hand, consumers have been responding overwhelmingly well to their offer.

And consumers, as we know, are always right.

This leap forward paid off: 10 years later, Visa and MasterCard’s business model is stronger than ever: both have almost doubled their transaction value and not a Canadian now walks on the street without hanging out, in their pocket, the logo of one or the other of the two big companies.

In the third part of this series, we will see how new developments, acknowledged by the secret memos, promise to change the dynamics of this industry in the near future, with or without a regulatory cap.